COSTA DEL SOL — INVESTMENT

How to Secure a Spanish Mortgage as a Non-Resident Buyer

our Expert Guide to Living and Investing on the Costa del Sol

For many buyers approaching the Costa del Sol property market from the UK, Ireland or Scandinavia, the assumption is that financing a Spanish purchase will be complicated, slow and probably not worth the effort. It is an assumption that costs more people more opportunities than almost any other misconception in the market. The truth is that Spanish banks actively lend to non-resident foreign buyers, the process — while different from what you may be used to at home — is well-established and clearly structured, and in 2026, with Euribor having fallen steadily from its 2023 peak of 4.16 percent to approximately 2.43 percent, mortgage rates for non-residents are considerably more attractive than they were just two years ago.

Understanding how the Spanish mortgage market works — its rules, its terminology and its requirements — is the single most powerful thing a prospective buyer can do before beginning their property search in earnest. The buyers who move quickly and confidently when the right property appears are almost always the ones who have done this preparation. Those who have not are the ones who lose properties to buyers who have.

“The buyers who secure the best properties on the Costa del Sol are the ones who have their financing ready before they start looking.”

What Spanish Banks Will Lend You

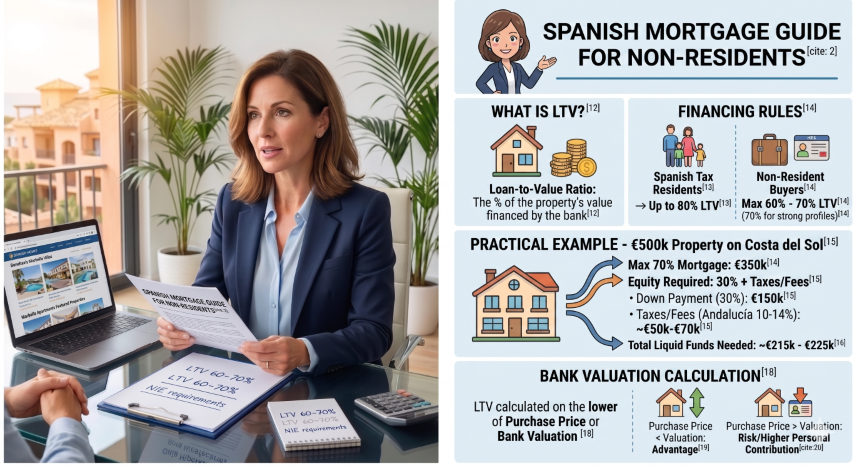

The starting point for any non-resident mortgage conversation is the loan-to-value (LTV) ratio — the percentage of the property’s value that a Spanish bank will finance. The rules here are clear and consistent: Spanish fiscal residents purchasing a primary residence can typically borrow up to eighty percent of the property’s appraised value. Non-resident buyers — defined as those who spend fewer than 183 days per year in Spain and pay their primary taxes outside the country — are offered a maximum of sixty to seventy percent LTV, with seventy percent available to buyers with strong financial profiles and clean credit histories.

In practical terms, this means that a non-resident buyer purchasing a €500,000 property on the Costa del Sol should plan to fund the remaining thirty to forty percent from their own resources — €150,000 to €200,000 — plus the full cost of taxes and professional fees, which in Andalucía typically run to ten to fourteen percent of the purchase price. On that same €500,000 purchase, a buyer at maximum LTV needs approximately €215,000 to €225,000 in liquid funds to complete the transaction comfortably. Having this number clearly in mind from the outset prevents the disappointment of finding the right property only to discover the financing does not stack.

Spanish banks calculate LTV on the lower of the agreed purchase price or the official bank valuation (tasación). If a property is being sold below its appraised value, the bank may lend against the higher valuation figure, which is a genuine advantage for buyers who negotiate well. Conversely, if the purchase price exceeds the valuation, the buyer must fund the difference from their own resources, which is an important risk to be aware of when buying in a market where demand is pushing prices ahead of formal valuations in some segments.

Spanish banks offer three principal mortgage structures. Fixed-rate mortgages provide payment certainty for the full term — typically up to twenty to twenty-five years for non-residents — and are particularly well-suited to buyers who will be managing payments from rental income and need predictability in their cash flow projections. Variable-rate mortgages offer lower initial rates and benefit directly from any further falls in Euribor, but introduce payment variability that some buyers find uncomfortable. Mixed-rate products, which start with a fixed period of three to five years before converting to a variable rate, have grown in popularity since 2024 as a hedge for buyers who want initial certainty while positioning for a lower variable environment.

Most Spanish banks also cap the loan term at the borrower’s seventieth or seventy-fifth birthday, which means younger buyers have access to longer terms and lower monthly payments, while buyers in their late fifties or sixties will typically be offered shorter terms of fifteen to twenty years.

“With Euribor at 2.43 percent in early 2026 — down from a peak of 4.16 percent in late 2023 — the rate environment for non-resident borrowers is the most favourable it has been in several years.”

The Documentation You Will Need

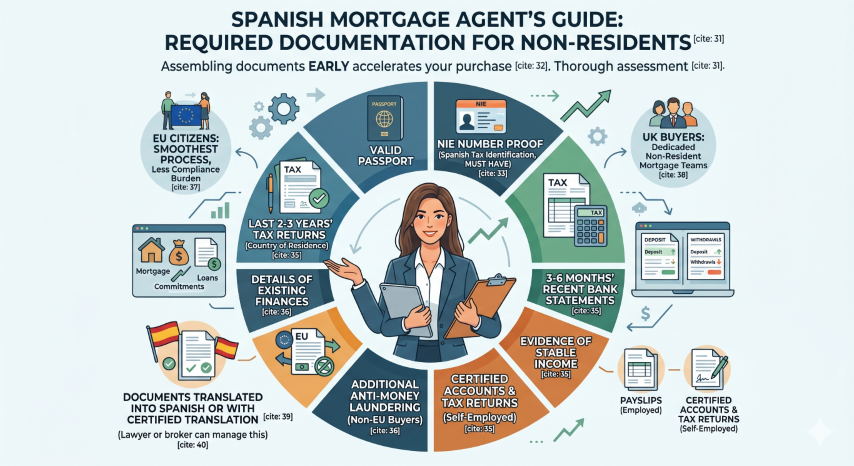

Spanish banks are thorough in their assessment of non-resident mortgage applications, and the documentation required is more extensive than most UK or Irish buyers are used to. Beginning the process of assembling your documentation before you find a property is the single most effective way to accelerate your purchase once the right opportunity appears.

You will need: a valid passport; proof of your NIE number (Número de Identificación de Extranjero, your Spanish tax identification number, which you must have before any property transaction can proceed); your last two to three years’ tax returns from your country of residence; three to six months of recent bank statements; evidence of stable income — payslips for employed buyers or certified accounts and tax returns for the self-employed; details of any existing mortgages, loans or financial commitments; and, for non-EU buyers, additional anti-money-laundering documentation that banks are now required to collect under strengthened 2026 regulations.

EU citizens benefit from the smoothest process, as common European data standards reduce the compliance burden. UK buyers, post-Brexit, sit in a slightly more document-intensive category but remain very well served by Spanish lenders, many of whom have dedicated non-resident mortgage teams. Most lenders will want documents translated into Spanish or accompanied by a certified translation; a good property lawyer or mortgage broker will manage this process on your behalf.

The Role of a Mortgage Broker

While it is entirely possible to approach Spanish banks directly, the majority of experienced international buyers on the Costa del Sol work with an independent mortgage broker who specialises in non-resident lending. The reasons are practical rather than commercial: a specialist broker will have established relationships with the lenders most active in the non-resident market, access to rates and terms that may not be advertised publicly, and the ability to identify which lender’s underwriting criteria best matches your specific financial profile.

Brokers also manage the bilingual communication process, translate documentation, liaise with the bank’s valuation team, and coordinate the mortgage timeline with your legal team and the developer or vendor. On complex transactions — particularly off-plan purchases, where the mortgage offer must align with the construction timeline — this coordination is invaluable. Most mortgage brokers on the Costa del Sol are remunerated by the lender rather than the buyer, making their services effectively cost-neutral to access.

The 2026 mortgage landscape on the Costa del Sol rewards buyers who are prepared, who understand the rules and who have assembled the right team around them. The financing is available, the rates are attractive, and the market continues to justify the investment. The question is simply whether you arrive at the property you want already mortgage-ready, or whether you arrive hoping to get there in time.

Thinking About Making the Move?

Our team of specialist advisors has been helping international buyers find their perfect home on the Costa del Sol for 15 years. Whether you are at the early stages of research or ready to view, we would love to hear from you.

T: +34 951 177 422 E: info@mosaicrealty.es W: www.mosaicrealty.es